Debts, derivatives and discipline

|

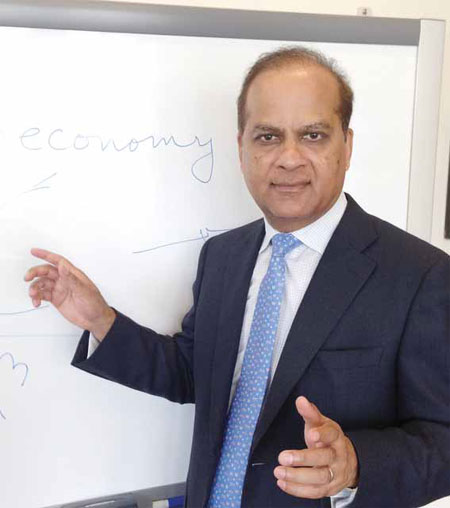

S. P. Kothari suggests the authorities curb easy credit and open up the financial services sector. Provided to China Daily |

Economist warns of potential financial crises in China and how to avoid them

With debts at local-government level mounting, China has to curb easy credit and open up the financial services sector to private and foreign enterprises, says S. P. Kothari, deputy dean of MIT Sloan School of Management.

Even as property prices continue to rise, some economists, including Kothari, have warned that the market is showing symptoms of the housing bubble in the United States that led to the economic crisis in 2008.

But the Chinese situation is unique, Kothari says, in that while people in the US were unable to repay loans and ended up defaulting, Chinese tend to buy homes with cash. The big problem is not with the buyers, but with the local governments.

Chinese local governments have been racking up debt due to large-scale constructions. They count on selling land to real estate developers to earn money, and therefore encourage them to develop properties.

"Once the debt crashes and the bubble bursts, the consequences will be similar - a financial storm," Kothari warns.

Kothari, formerly head of global equity research for Barclay's Global Investors, and head of the economics, finance and accounting department at MIT Sloan in Cambridge, Massachusetts, is now in charge of the school's international programs. He came to Beijing recently to launch the global MBA program with its long-time partner, the School of Economics and Management at Tsinghua University.

"If there is too much housing built but not enough people to occupy it, there will be problems," he says. "This is not the situation yet in big cities, in Beijing, Shanghai or Guangzhou, but in many other places, the risk already exists."

He warns the government not to provide easy credit, either to home-buyers or real estate developers.

"The government tries to stimulate the economy by issuing more debts - basically, it is like printing money," he says. "(In the US) after 2001, the government made it very easy for people to buy homes and it pushed up the prices. But once the prices dropped, a lot of people previously involved in construction lost their jobs, so people unable to pay back the loans began to default."

China's National Audit Office estimates that local debt will total 15 trillion yuan to 18 trillion yuan ($2.9 trillion; 2.2 trillion euros) in 2013, and some international organizations estimate it will be much larger.

Issuing debt is helpful if there is short-term liquidity problem, "but politicians use this method too much", Kothari says.

"China is still growing, and there is still huge demand for construction because the manufacturing industry is taking off and there are large numbers of people migrating from rural to urban areas. But the government has to grow with more market discipline."

It needs to open up more to private enterprise in the service sector, especially the financial sector, to create a more vibrant economy and reduce dependence on manufacturing and real estate industries.

"China needs a more diversified economy and that's why in Western countries the financial services are bigger than many other segments. Services such as those within the culture industry, entertainment industry and financial industry have to be more prominent in China's economy."

The banking system in particular needs to involve more private and foreign companies, Kothari believes, as China's state banks don't manage risks well enough - partly because they know there is government backup.

"Because the government can make cash available and banks know the government will make money available, there are many non-performing loans in the state banks. It is almost like they default, but they are not penalized. We cannot rely on government supervision to improve the banking system."

Private financial service providers will be more careful before lending because it's their own money; and if there is default, they will be persistent in collecting money, he says.

"And the government, instead of pumping money into real estate industry, can make investment in other segments that might be more fruitful."

Kothari says the Chinese government has to be decisive in believing this is the right thing to do for the long-term good of the country.

When talking about opening up the financial sector, derivatives cannot be avoided, Kothari maintains, disagreeing with some economists who claim they are "weapons of mass destruction".

"It's easy credit, not the derivatives, that causes the financial crisis," he says. "The housing problems in the US were concentrated in California, Nevada, Arizona and Florida, where easy credit is biggest."

If derivatives are the problem, he adds, it is strange that Germany, a big user of the contracts, has not been affected as severely in the financial crisis, whereas Spain and Greece, who do not go in for derivatives, were badly hit.

"For the size of China's economy, it should have a very vibrant derivative market," Kothari says.

He suggests the government introduce a whole batch of derivatives at one time.

"Many derivatives link, so you cannot have one but not another. It's like if you have a buffet, you cannot offer only one or two dishes. If you have debt-related derivatives, you have to have currency-related derivatives."

The stock market also needs to be reformed, Kothari says.

He doesn't agree with analysts who say the Chinese stock market is poor because Chinese investors don't have the insight for long-term investment but prefer short-term speculation.

"In the US from 1968 to 1982, the stock market was basically flat. In Japan, the Nikkei Index was almost 40,000 in 1989, and it is 14,000 today. So it is normal that the stock market fluctuates. But China has been growing so rapidly and the stock market shouldn't be so low."

He says the Chinese authorities should make it much easier for foreign investors to buy stocks to break this deadlock.

"Nobody in the US asks which country you belong to if you want to buy stocks, but foreign investors are locked out of Chinese stocks.

"China has opened the manufacturing segment - it is very easy for General Motors to come. It also attracted much foreign direct investment. But now the focus is more and more on services.

"If you have more players from foreign countries, it is much more difficult to manipulate the stock prices."