Private banks to ignite healthy rivalry

Policymakers get the ball rolling on a key reform that will improve service and efficiency in banking

The approval of private banks, announced on July 25, could be deemed the year's most important development for China's financial sphere, if not for the whole economy.

The move underscores policy determination, breaks up state monopoly, helps alleviate funding problems for small and medium-sized enterprises and will help foster a multilayered financial market.

The central leadership seriously began to consider allowing private investors to set up banks in 2012, when then-premier Wen Jiabao criticized state banks for raking in easy money by exploiting their monopolistic position. Starting then, policies were mapped out and preparations made for allowing private banks.

Banking reform accompanies central authorities' decisions to promote mixed-ownership reforms and allow private investors to play a bigger role in other state-controlled industries.

But worries emerged recently that reforms might slow as top leaders seemed to attach more importance to economic growth since the end of the first quarter. China's GDP growth hit 7.4 percent in the first half of the year, below the yearly target of 7.5 percent. The slowdown gave rise to speculation that growth would overtake reform as the top priority.

However, the July 25 banking move puts paid to the conjecture. The move demonstrated that reform will not be sacrificed because of slower growth.

This display of determination is vital, given that local governments are watching the stance of the central government. Any hesitation or indecisiveness would harm future reform efforts. Breaking the state banking monopoly has long been regarded as a tenet in China's economic reform. But with the go-ahead for private banks, the central leadership's message is loud and clear: No matter how arduous, reform will go ahead.

Before the green light was given, private investors had already been allowed to invest in banks of all sizes. For example, two major national banks - China Minsheng Bank and China Merchants Bank - have seen private capital absorb a large chunk of their ownership. There are also many city commercial banks that have private investors as major shareholders. But these banks are still controlled by the government in one way or another. The government appoints their executives, and operations are subject to government intervention. Private stakeholders have little significant say in banks' decision making or operations.

This scenario will change with the establishment of the first real private banks. Three banks - in Shenzhen, Wenzhou and Tianjin - are backed by private companies, according to authorities. They will have a full say in the operations of the banks. In this sense, they will be the first genuine private banks in China.

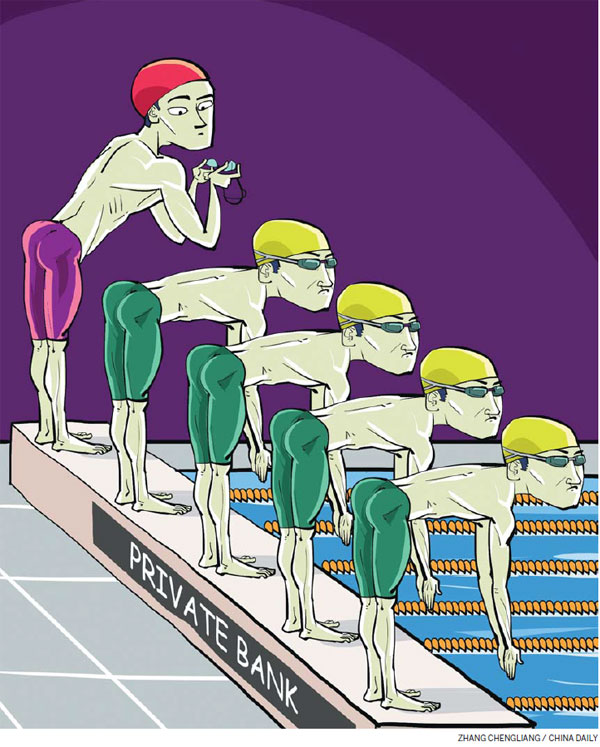

The emergence of these banks will inject competition into the tightly state-controlled sector. Although the state monopoly cannot be significantly shaken, private banks will crack open their state peers' total control.

Private banks will most likely begin with financing small to medium-sized enterprises, innovation and services. Their success will push larger state counterparts to change and improve.

Unlike state-owned giants, private banks are naturally drawn to smaller enterprises. If a bank's stakeholders are mostly private business owners who have built their wealth from scratch, they will have a better understanding of small business and an innate friendliness toward them.

State banks tend to serve large, government companies, because these lenders believe that small and medium-sized firms, without a strong background and financial brawn, are prone to default.

But with business acumen and a well-developed information network in the local market, private banks can excel serving that market.

More importantly, private banks will often have a creativity gene, thanks to the participation of Internet companies. Internet giant Tencent Holdings is among the major stakeholders of the private bank in Shenzhen. Alibaba Group is expected to join the next group of private banks.

Players like Tencent and Alibaba have huge customer bases, sound and complete databases of small businesses, respected reputations and strong technological capabilities. Their participation is expected to encourage better service to smaller businesses and individual investors, and to help develop more creative financial products.

One recent example of private Internet companies forcing state peers to change was the work of giants in the field, including Alibaba, Baidu and Tencent. Their money-market funds, backed by traditional fund managers, won the hearts of hundreds of millions of small investors with their high liquidity, handsome return rates and greater investor convenience. The funds helped small investors bypass the deposit ceilings established by traditional banks. This prompted some banks to introduce similar financial products.

Another example of how Internet companies can help smaller firms with financing came last month, when Alibaba launched an unsecured loans program. Small and medium-sized enterprises can apply for a credit line of up to 10 million yuan ($1.6 million), from several banks, such as Bank of China, China Merchants Bank and China Construction Bank, based on records tracking their trustworthiness in Alibaba's database. The loan rate is no more than 8 percent, not a very high rate for smaller businesses. Such businesses in China often pay annual interest of 12 to 15 percent. Alibaba has not received approval to set up its own bank, so it has to work with other banks. But if Alibaba gets a banking license, it can grant loans by itself, which will create competitive pressure for state banks.

For the time being, private banks will not grab too much market share from state banks because private banks will mostly serve smaller firms, which are not the state banks' major customers. But when these private banks' customer bases grow, they will eventually step on the turf of large state banks.

This will force state lenders off their high horse and make them improve their service and cut interest rates to woo customers.

Clearly, with more private banks popping up in the future, China's banking sector will change, with a boost in overall efficiency.

But there are a few things worth noting.

The first private banks are all in coastal areas, even though central and western parts of China deserve at least a seat at the private banking table. With industrial relocation, inland China now also faces severe financing problems. Because of an undeveloped financial market, local small and medium-sized enterprises have even fewer ways than their coastal counterparts to access capital. Many inland private companies have ties to agriculture and need banking deregulation to help farmers and farm companies.

It is also important that insider lending be strictly checked at private banks.

One concern is that stakeholders of private banks may see the banks as their private coffers and ask them to lend to sister companies for investment in high-risk areas.

Such practices need to be avoided. A private bank's loans, directly or indirectly, to its stakeholders, be they companies or individuals, should be limited. Its ratio of loans to a single customer, now set by the government at 10 percent for all lenders, could be capped at a lower percentage. Such measures will help prevent the banks' loans from flowing back to its stakeholders, who might use the money for speculation.

The authors are Shanghai-based financial analysts. The views do not necessarily reflect those of China Daily.