China's biggest banks still dominate the world's top 10 in terms of market capitalization and are among the most profitable globally, according to a report by Boston Consulting Group.

But their falling valuation multiples suggest declining investor confidence in their future profitability.

Driven by rapid growth in credit spreads, China's big four banks all made it to the list of the world's top banks, with Industrial and Commercial Bank of China maintaining the top spot, while China Construction Bank, Agricultural Bank of China and Bank of China took the third, sixth, seventh positions.

Four US banks also made it into the top 10 list.

China's banks are among the most profitable, with an average of 22 percent after-tax return on equity (ROE), second only to that in Indonesia, where ROE was 26 percent.

However, Boston Consulting suggested that the high profitability of China's banks was unlikely to be sustainable, evidenced by falling price to book values and price-earning ratios.

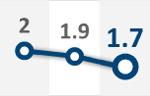

The price to book ratio — a key indicator of whether a public company is undervalued or overvalued — of Chinese banks fell from the record high of nearly five in 2007, to just above one.

By contrast, banks in Indonesia, Mexico and India, registered a similar ROE-COE (cost of equity) level as China's, but enjoyed a much higher price to book ratio.

China's banks' price-earning ratio also fell from the record high of over 30 to below 10.

Ranu Dayal, a BCG senior partner and co-author of the report, said: "Clearly there is a lack of faith in China's economy, and in the level of hidden losses or likely potential losses.

"The single most important thing for Chinese banks to do is to increase transparency and improve loan books, to show how (loans) are actually performing, and what's not.

"Better transparency will likely increase investor confidence, which should lead to an improvement in valuation," Dayal said.

"Without that, there is increasing skepticism that the ROE is likely to fall in the future."

The BCG report also suggests that China's banks should evolve their business models as soon as possible, amid the context of an economic slowdown and interest rate liberalization.

"The past 10 years was the golden era for China's banking industry, but there is no reason to indulge on that," added Richard Huang, a partner and managing director of BCG.

"Thanks to China's interest rate system, its banks in the past 10 years had enjoyed a stable interest rate spread, and that spread single-handedly contributed to their rosy profit."

But as the local economy enters a downward cycle, while interest rates have become increasingly liberalized, Huang said it was time to see who is "swimming naked" in the ebbing tide.

He added: "The strong cyclical development model that heavily relied on traditional corporate credit will need to evolve — China's banking industry must seek new business opportunities and adjust its business model."

With that adjustment in mind, the report suggests China's banks draw lessons from the practices being used by some in developed economies, which continue to perform well against a bleak overall financial market.

It uses Wells Fargo, the US bank that ranked second in the list, as an example of being able to outperform traditional giants because of a business model which focuses on developing retail business and accumulating low-cost deposits.

Two other organizations it highlighted were Visa and MasterCard, which have benefited from a stable revenue stream from payments and transactions, according to the report.

But Dayong He, a BCG principal, cautioned that "going global" might not necessarily be a good strategy for all Chinese banks, using those in Canada and Australia as examples.

Banks there — which have not historically followed the rapid global expansions of some Western counterparts — managed to keep their profitability at fourth and fifth in the world, as profits in the West fell sharply amid the eurozone debt crisis.

That was proof, the report added, that "focusing on a strong and stable domestic market" can be highly profitable.

"From a global perspective, the Chinese mainland is still one of the most attractive markets, and enjoys strong vitality. Therefore, domestic banks should seize the opportunity to strengthen the foundations of their leading domestic positions," Huang said.

Contact the writer at zhengyangpeng@chinadaily.com.cn

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()